Domestic aluminum scrap prices continued to climb this week, with single-day adjustments in some regions reaching 300 yuan/mt. As of September 4, the SMM A00 price closed at 20,860 yuan/mt, up 250 yuan/mt WoW. Supply in the aluminum scrap market remained tight, particularly for aluminum tense scrap resources, where prices stayed firm, with mainstream offers excluding tax hovering between 17,300-17,800 yuan/mt. Baled UBC prices, supported by rigid demand, fluctuated within the range of 15,650-16,150 yuan/mt. Regional trends diverged; since September, Jiangxi and Hunan significantly raised recycling prices due to supply tightness, with cumulative increases of 400 yuan/mt, while east and central China mostly adjusted in line with aluminum price gains. Operating rates at downstream secondary aluminum enterprises rebounded mildly, but the peak season demand characteristics of "September peak season" have not fully materialized, resulting in a supply-demand mismatch in the market. Aluminum scrap prices are expected to hover at highs next week, with intensified negotiations between sellers and buyers. From a macro perspective, the cleanup of irregular tax rebates across regions continues. Although policies are still in a transition period and current purchasing offers do not yet reflect their impact, medium and long-term, scrap utilization enterprises may bargain down purchasing prices to pass on rising tax costs, posing a downside risk to aluminum scrap prices. On the other hand, the tight supply situation is unlikely to improve in the short term, particularly for shredded aluminum tense scrap, which will continue to give suppliers bargaining power. SMM expects the mainstream range for shredded aluminum tense scrap (including moisture) to fluctuate around 17,300-17,800 yuan/mt, while baled UBC prices will hover between 15,600-16,100 yuan/mt. The market needs to closely monitor the implementation progress of tax policies and the actual recovery of downstream consumption, as price trends will depend on the balance between cost transmission and supply tightness.

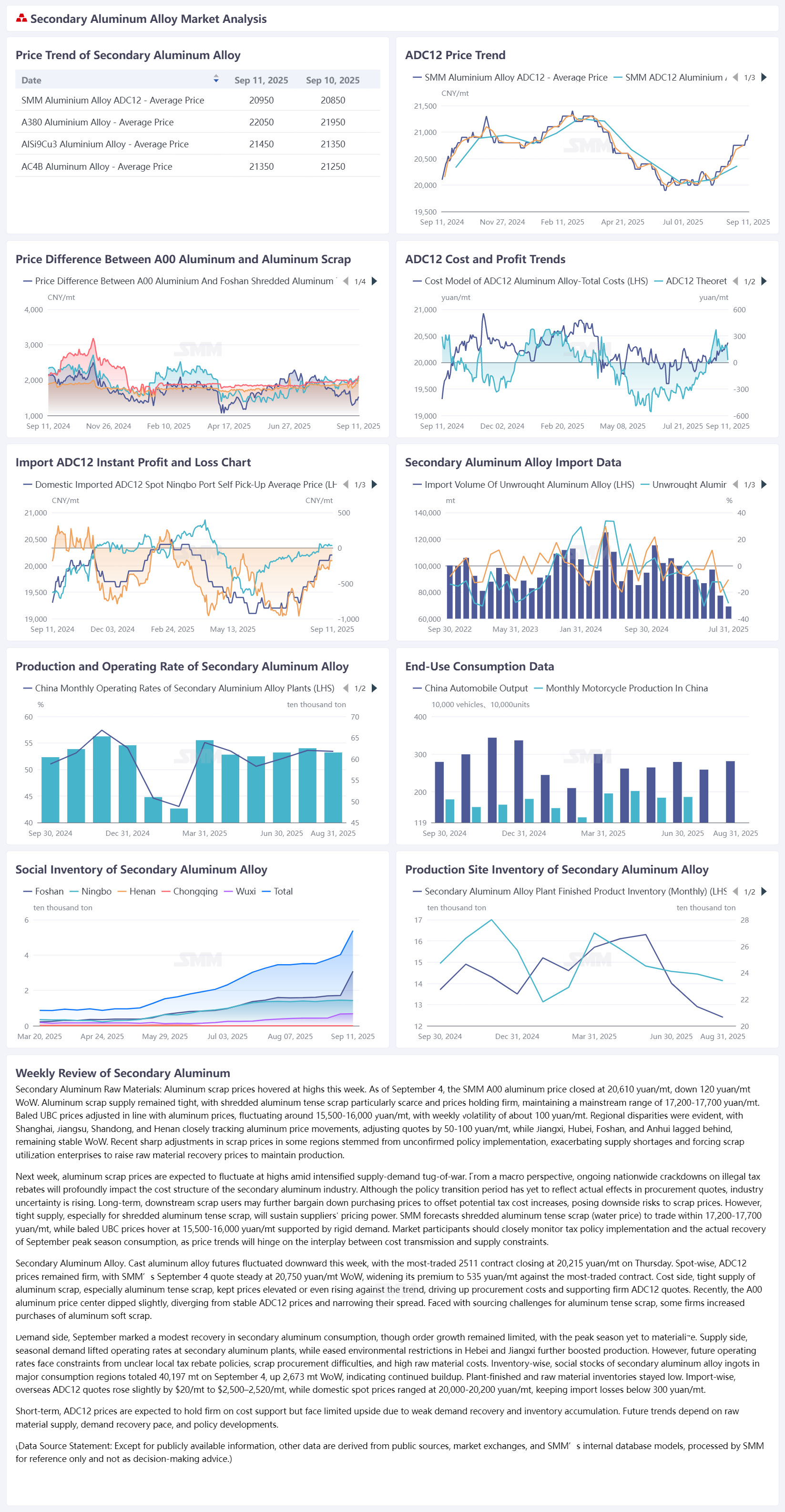

This week, cast aluminum alloy futures fluctuated upward, with the most-traded 2511 contract closing at 20,475 yuan/mt on Thursday. In the spot market, ADC12 prices continued to hold up well. As of September 11, the SMM survey quoted the price at 20,950 yuan/mt, up 200 yuan/mt WoW, maintaining a premium of 500 yuan/mt against the most-traded contract. Cost support strengthened significantly. Due to tight domestic and overseas aluminum scrap circulation resources and increased demand from scrap utilization enterprises, the aluminum scrap market shortage intensified, with hoarding pushing prices up rapidly. To ensure order delivery, some manufacturers made high-priced or even cross-regional purchases. Rising costs further boosted ADC12 prices and maintained its premium over A00 aluminum. Demand side, downstream procurement sentiment recovered slightly since September, with demand continuing to rebound, but the actual strength of the traditional peak season remains to be verified. Facing dual pressures of raw material shortages and low finished product inventories, some secondary aluminum enterprises became more cautious in taking orders, even intentionally controlling order sizes to avoid falling into a "more production, more losses" dilemma. Supply side, the SMM survey showed that the operating rate of leading secondary aluminum enterprises rose slightly by 0.3 percentage points WoW to 53.5%, mainly driven by improved consumption. However, the industry overall is still constrained by insufficient raw material supply and policy uncertainties. In the import market, overseas ADC12 offers rose slightly by $10/mt to $2,500–2,530/mt, while domestic spot prices traded at 20,100–20,300 yuan/mt, up 100 yuan/mt over the week. Affected by the stronger RMB exchange rate, the immediate import loss narrowed to within 200 yuan/mt. Overall, ADC12 prices are expected to continue fluctuating at highs in the short term supported by costs, but limited demand recovery and increasing social inventory will still cap upside room. Follow-up focus should be on raw material supply conditions, demand recovery progress, and potential policy impacts on the market.